The Audit Exemption They Buried in the Fine Print

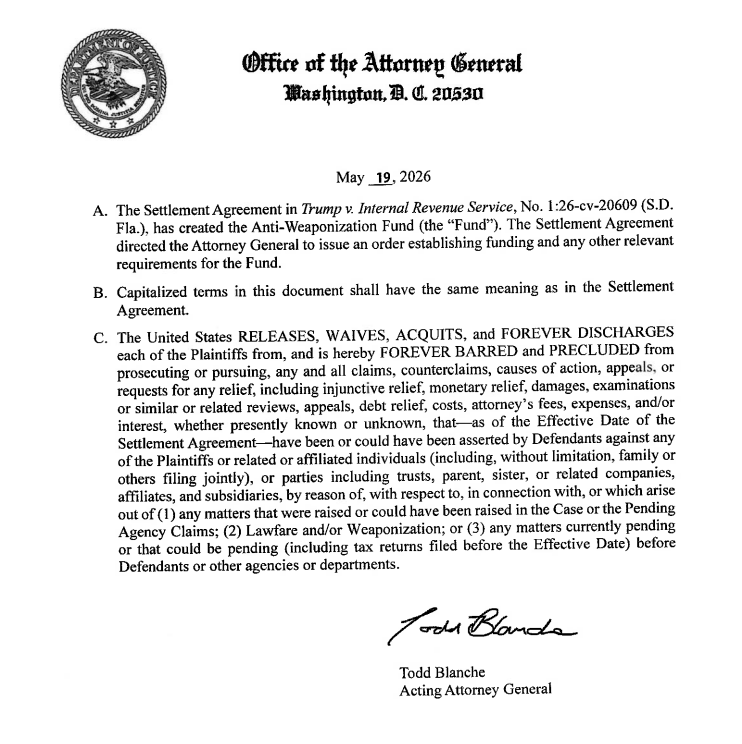

The $1.8 billion Anti-Weaponization Fund dominated headlines. The one-page addendum posted the next day permanently bars the IRS from auditing Trump, his family, and the Trump Organization, closing an active $72.9 million dispute. That part was quieter. It was designed to be.

The $1.8 billion “Anti-Weaponization Fund” is the headline. The one-page addendum posted the next day is the story.

THE GAP

What the Coverage Led With

The Justice Department announced a $1.776 billion fund on Monday, framed as compensation for Americans who say they were politically targeted by the Biden administration. Acting Attorney General Todd Blanche called it “a lawful process for victims of lawfare and weaponization to be heard and seek redress.” The number, $1.776 billion, was chosen deliberately, a reference to 1776, American independence rendered in taxpayer dollars.

The announcement came packaged as a settlement: Trump and his family dropped a $10 billion lawsuit against the IRS over the leak of his tax returns. In exchange, the fund was created. Democrats called it a slush fund. Republicans like Senate Majority Leader John Thune said they were “not a big fan.” The story cycled through the usual outrage loop.

Most coverage stopped there.

What Got Buried

A one-page document quietly posted to the DOJ website the following day changed the terms significantly. The expanded waiver declared the IRS is “forever barred and precluded” from prosecuting or pursuing any and all claims related to Trump or affiliated individuals, covering all tax returns filed before the settlement date. Only Blanche, who previously served as Trump’s personal criminal attorney in three federal cases, signed the document blocking Trump, his family, and businesses from facing tax audits. The press release issued Monday announcing the settlement made no mention of it.

The fund was the distraction. The audit exemption was the delivery.

Why the IRS Knew Better

A leaked 25-page IRS memo shared with Treasury officials showed the agency’s own lawyers believed Trump’s original lawsuit was deeply flawed. Federal statute requires IRS suits to be filed within two years of the alleged infraction. The memo noted that Alina Habba, one of Trump’s personal attorneys, was present at the trial of IRS leaker Charles Littlejohn in October 2023, establishing that Trump’s team had knowledge of the leak well before claiming otherwise. The lawsuit was, by the IRS’s own legal analysis, dead on arrival.

The DOJ settled anyway.

ROOT

The One Carve-Out That Made It Legal

Federal law prohibits the White House from directly instructing the IRS to start or stop specific audits. That protection exists precisely because tax enforcement over a sitting president is a structural accountability mechanism, not a political favor. The Justice Department did not address a criminal law, now being raised by critics, that prohibits presidents and other executive branch leaders from requesting the termination of IRS audits. The carve-out that allows the Attorney General to act became the door. Blanche did not act as an independent law enforcement officer here. He is the man who previously served as Trump’s personal defense attorney in the federal cases over the 2020 election and the classified documents, negotiating a settlement with an administration he now serves, shielding a president he previously defended, from a tax enforcement process he now controls.

How the Fund Is Structured to Stay Unaccountable

The Anti-Weaponization Fund will be overseen by a five-member commission appointed by the Attorney General. The President can remove any member, with a replacement chosen through the same process. No detailed eligibility standards have been released. When Blanche was pressed in a Senate hearing on who qualifies, his answer was “anybody in this country can apply,” with a commission yet to be formed deciding the rules. The DOJ’s own press release notes the fund “can be audited,” at the Attorney General’s direction. The fund that shielded the president from audits can only be audited by the man who signed the shield.

The Attorney General’s Conflict of Interest Is the Architecture

The Treasury Department’s own General Counsel resigned the same day Treasury was required to certify the fund payments. When Blanche was asked whether the resignation was a coincidence, he said “I don’t know if it’s a coincidence,” adding that he had not checked why it happened. A senior legal officer at Treasury walked out the day the money moved, and the acting AG responsible for the transaction did not look into it. That is not a coincidence story. That is a resignation-of-conscience story, the kind institutions produce when someone with legal exposure decides they would rather leave than sign.

WHO PROFITS

The First Applicant Was Already in Line

The first known compensation request came the day after the announcement, from former Trump adviser Michael Caputo, who sent a letter seeking $2.7 million, claiming harm from the FBI’s investigation into Russian interference in the 2016 election. Caputo did not wait for eligibility rules. There were none to wait for. Jan. 6 defendants, including those convicted of assaulting police officers before being pardoned by Trump on his first day back in office, are widely expected to apply. Blanche declined to rule out payments to members of the Proud Boys or Oath Keepers. A publicist who represents Jan. 6 defendants told CBS News that “anyone targeted by the Department of Justice will want to submit.”

What the Audit Shield Is Actually Worth

Most coverage treated the fund’s $1.8 billion as the headline number. The personal financial value to Trump runs through the audit exemption, not the fund. The settlement likely eliminated a dispute over a $72.9 million tax refund Trump claimed as host of The Apprentice. The trade was structured so the public sees a $1.8 billion payout to “victims,” and the president receives quiet, permanent protection from an audit process that had an active nine-figure dispute attached to it. No direct payment to Trump. No record in court. The judge overseeing the original case noted there is no official settlement of record, writing “because the Notice does not reference any settlement or include a stipulation of settlement, there is no settlement of record.” The deal exists, the money moves, and there is no court document to challenge.

Loyalty as the Operating System

Nine days before the fund was announced, Trump publicly demanded loyalty from the Supreme Court justices he appointed, calling those who ruled against him on tariffs “unpatriotic and disloyal.” CNN noted the episode would have been a career-ending scandal in his first term. In his second, it barely registered. The pattern connecting those two moments is not temperament, it is architecture. The Attorney General who signed the audit exemption was Trump’s personal defense lawyer. The commission overseeing the fund is appointed by that same AG and removable by the president. Legal experts say critics have no clear path to challenge it in court because there is no obvious plaintiff. Federal precedent does not recognize taxpayer standing, meaning everyone is harmed and the government does not recognize that harm as legally actionable. Loyalty is not a value being expressed here, it is the selection mechanism determining who enforcement reaches and who it does not. The fund is not a reward. The audit exemption is not a side effect. Together they are the transaction, paid for by everyone who still has to file.

The Enforcement Mechanism Was the Point

Accountability for concentrated wealth in the United States runs through very few institutional channels. The IRS is one of them. It does not require a criminal conviction. It does not require political will from a Congress that has spent decades defunding its audit capacity. It operates on returns, documentation, and statute. For the wealthiest and most powerful, the audit is often the only enforcement mechanism left.

That mechanism, for the Trump family and the Trump Organization, was permanently closed this week. Not suspended, not delayed, forever barred by the signature of a man who used to be their lawyer.

Where the Leverage Is

Calling your representative is not useless, but it is also not sufficient for a deal structured to avoid judicial review entirely. The most viable legal path forward is a False Claims Act challenge, which requires a whistleblower inside the process to come forward with documentation of fraudulent claims being paid. The FCA’s qui tam provision allows a private citizen to file on behalf of the government and collect 15 to 30 percent of any recovery, filed under seal to protect the whistleblower during investigation. That is a real mechanism with legal teeth and financial incentive attached. If you work in government, law, or finance and have proximity to this fund’s operations, that avenue exists and attorneys will take these cases at no upfront cost.

For everyone else, two organizations have active legal infrastructure and the standing to pursue this in court: Citizens for Responsibility and Ethics in Washington and Democracy Forward. Financial support to either is more direct than most other actions available right now. The 93 House Democrats who filed an amicus brief challenging the settlement as an unconstitutional collusive lawsuit have already laid the constitutional groundwork, arguing Trump cannot be plaintiff and president simultaneously. The question is whether organizations with standing can get into court before the money moves within 60 days.

The last thing worth understanding clearly: the standing trap is not an accident. A deal structured to bypass judicial review, with a commission appointed and removable by the president, with no public record in court, is a deal designed to be unchallengeable by the people paying for it. Knowing that is not despair. They built it to be unchallengeable. That has never, in the full sweep of this country’s history, been the last word.

FURTHER READING

- DOJ Anti-Weaponization Fund press release, Department of Justice

- Leaked IRS memo analysis, The New Republic

- IRS settlement expanded to bar Trump tax audits, Axios

- Why critics have no clear path to challenge the fund, Semafor

- Trump legal deal draws bipartisan scrutiny, Washington Post

- Full constitutional analysis of the fund, Mitch the Lawyer / Substack

Our Revolution Media is an independent publication covering labor, power, and political economy. Subscribe at ourrevolution.media.